US GDP Falls Short of Expectations and Inflation Rises: A Closer Look at the Numbers

Abstract:Gross domestic product (GDP) in the United States represents the total aggregate output of the U.S. economy. It is important to keep in mind that the GDP figures, as reported to investors, are already adjusted for inflation.

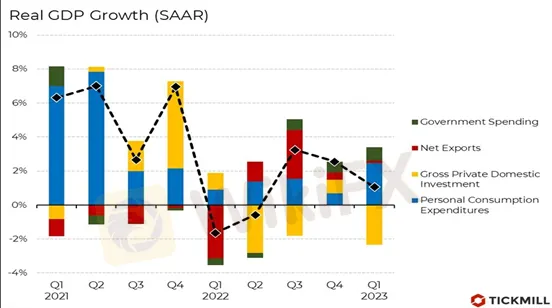

Gross domestic product (GDP) in the United States represents the total aggregate output of the U.S. economy. It is important to keep in mind that the GDP figures, as reported to investors, are already adjusted for inflation. The risk appetite in global markets came under pressure while safe-haven demand increased after the US GDP and inflation data on Friday. For the first quarter, the US GDP posted a big “bearish” surprise, rising by only 1.1% compared to the forecast of 1.9%. Looking at the GDP separately for the four main components (consumption, investment, government purchases, and net exports), it is evident that it was the investment component that dragged down the headline reading while consumption and government purchases maintained a good positive momentum:

In annual terms, consumption grew by 3.7%, with a strong jump in January when unusually warm weather stimulated early activity rebound after December. Government purchases increased by 4.7% in annual terms, and net exports added 0.11% to the annual GDP growth rate.

However, the deficiency of the main indicator was hidden in downside momentum of investments (21% of GDP). It consists of three main components: investments in fixed assets, firm inventories, and households' residential investments. While firm investments in fixed assets grew by 0.7% (quite weakly), investments in housing decreased by 4.2%. In quarterly terms, this indicator has been decreasing for 8 consecutive quarters due to pressure from mortgage rates combined with sticky high housing prices that accelerated during the period of low rates after the pandemic. Firms also reduced their inventories in the first quarter (which is considered negative investment), which took away 2.26 percentage points from the GDP growth rate.

As for inflation, the core GDP deflator (one of the inflation metrics) increased by 4.9% on an annual basis, up from 4.4% in the previous quarter and above the consensus of 4.7%. Along with disappointment over the GDP data, the market was forced to reprice the risks of the Federal Reserve's monetary policy tightening in light of hawkish inflation data for May 1. The rise in Core PCE exceeded expectations - 4.6% versus the forecasted 4.5%. The February figure was revised upward to 4.7%. Monthly inflation was in line with expectations at 0.3%.

In the next quarter, consumption is likely to make a less significant contribution to GDP, given recent consumer trends (decline in retail sales). Weak investments suggest a reduction in corporate optimism about the short-term prospects of the US economy. CEO surveys of US companies and the NFIB small business index indicate preparations for a downturn and recession, which will further depress hiring and investment in capital goods.

The consensus for Q2 GDP growth is shifting closer to 0, and the actions of the Fed, which is forced to fight inflation, will likely bring the onset of a recession in the US economy closer. Also, we cannot underestimate the possibility of new banking shocks, which could lead to a sharp tightening of credit conditions and further hit economic activity.

The dollar received a boost on May 1 due to increased demand for the US currency as a safe haven asset. Looking at the EURUSD pair, it can be seen that the price is consolidating around the lower boundary of the uptrend channel, which can be seen as a signal that the uptrend may be petering out and closer to the Fed meeting, there may be a break downward:

Read more

Indian Stocks Rally, but the Rupee Breaks a Six-Day Winning Streak—What's Behind the Sudden Reversal

Indian stock indices today, i.e., June 22, 2026, recorded growth, with the BSE Sensex rising 297.11 points to 77,094.07, recording a 0.38% jump. On the other hand, the NSE Nifty hit approximately 24100, largely aided by broad-based purchases across sectors, except for consumer durables and fast-moving consumer goods (FMCG). The Nifty grew by 89.80 points (0.37%+) to 24,102.90.

Telegram Banned in India? Here's What Traders Must Do Next

Yes, it’s true! The Government of India decided to ban Telegram in the country on June 16, 2026, surprising many who rely on this platform for daily trading alerts & advisories. The ban has taken effect under Section 69A of the IT Act as part of the government’s plan to stop fraud during the NEET-UG re-examination. According to reports, fraudulent rackets were selling fake question papers for amounts ranging from INR 5,000 to 50,000. But the ban, which will be effective until June 22, 2026, affects far more than students. It transcended from a messaging blockout to a sudden disengagement from the app that shaped many traders’ daily routine over time. Out of the 15 crore plus unique registered investors in India, a large chunk sought trading tips, market news, along with buy and sell signals on Telegram. It must have taken investors by surprise. But is the ban detrimental to traders, or is there something more than meets the eye?

iFOREX Europe Review 2026: Fund Withdrawal Complaints Keep Pouring Year After Year

As we look to sum up iFOREX Europe and check user comments, they all read virtually the same issue, year after year - fund withdrawal issues. While some users never received withdrawal access from the broker, others received it for some time before the trading enterprise suspended their trading account, leaving their funds allegedly trapped on the platform. In this iFOREX EUROPE review, we take a close look at reported fund scam allegations against the brokerage first. Additionally, we will elaborate on the broker’s product & services and its regulatory framework.

Rupee Climbs to a Six-week High Today - Is the Bad Time for the Currency OVER?

The rupee, which has been falling against major global currencies, including the US dollar, is finally back on the path to recovery. As per the initial trade, the rupee touched a six-week high of 94.43 against the USD on June 17, 2026, tracking a plunge in crude oil prices following the interim peace deal agreed upon between the United States of America and Iran. Brent crude oil price slipped to around $78 per barrel, which has not been the case for three straight months following the war. The surging crude oil prices further caused pressure on the rupee, which was already falling apart.

WikiFX Broker

Latest News

Review 2026: Deriv Regulation, Complaints, and Withdrawal Risk Signals

WikiFX

WikiFXStop Trading in the Middle of Ranging Forex Markets

WikiFXRoboMarkets Review: Regulation Questions Around a Broker Facing Fresh Trading Complaints

WikiFXSTONE WALL CAPITAL Review 2026: Is This Forex Broker Safe?

WikiFXFinalto Review 2026: Regulation, Trading Environment, and Platform Access

WikiFXFXTF Review 2026: FSA Regulation, MT4 Access, and Mixed Trader Reports

WikiFXErrante Review: Regulation Alarms and Broker Complaints Traders Cannot Ignore

WikiFXBaFin Issues Fresh Warnings Over Unauthorized Financial and Crypto Services

WikiFXMetaTrader 5 Expands Infrastructure With New Amsterdam Hosting for Backup Servers

WikiFXUnderstanding Day Trading: Fast Decisions, High Stress, and Zero Overnight Risk

WikiFXRate Calc