Yields Rise, Rate-Cut Odds Slide As ISM Services Survey Signal Inflation Fears

Abstract:After yesterday's mixed picture on Manufacturing (PMI up, ISM down), analysts expected both Services

After yesterday's mixed picture on Manufacturing (PMI up, ISM down), analysts expected both Services surveys this morning to show an upward bounce.

- S&P Global's Services PMI disappointed but did risefrom September's 54.2 to 54.8 (but that was less than expectedand less than the 55.2 preliminary print)

- ISM's Services PMI beat expectations, rising from 50.0 to 52.4, well above the 50.8 expectations.

And this is happening amid a rise in 'hard' data (though admittedly based on housing and marginal labor data given the vacuum since the shutdown)

Source: Bloomberg

Across the PMI surveys, only ISM Manufacturing saw a decline MoM in October...

Source: Bloomberg

Under the hood,Prices surged to their highest in three years, new orders expanded at their fastest pace in a year and employment improved (though remained below 50)...

Source: Bloomberg

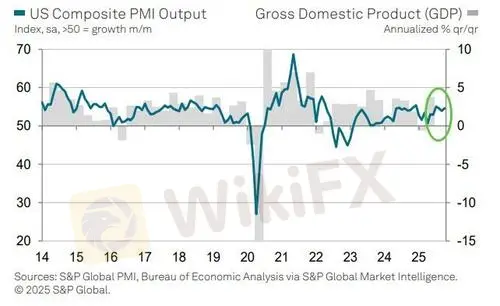

Octobers final PMI data add to signs that the US economy has entered the fourth quarter with strong momentum, according to Chris Williamson, Chief Business Economist at S&P Global Market Intelligence.

While growth is being driven principally by the financial services and tech sectors, Williamson says the survey is also picking up signs of improving demand from consumers.

However, the surge in prices paid is having some consequences

Business expectations about the year ahead have also fallen sharply and are now running at one of the lowest levels seen over the past three years, as Williamson notes “signs of spending caution from customers is accompanied by heightened political and economic uncertainty.”

However, Williamson points out that lower interest rates have helped offset some of the drags to business confidence, for which the October FOMC rate cut will have likely helped further.

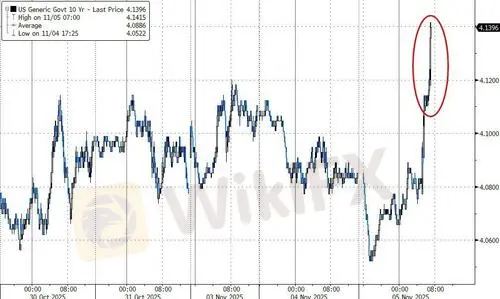

Treasury yields are on the rise (likely driven by the inflation jump) and rate-cut odds are lower...

Hopefully we will get some 'hard' data reality (Payrolls and CPI) if the government reopens before the next FOMC meeting but for now we would say, this should not be weighted enough to warrant The Fed veering from its easing path.

WikiFX Broker

Latest News

Alpari Review 2026: Official Warnings and High Complaint Patterns

WikiFXM4Markets Broker Review: Regulation, Licenses and WikiScore Analysis

WikiFXOver RM102 Million Crypto Seized in Romance Scam Crackdown

WikiFX"High Inspirations" Mastermind Disappears as $25 Billion Investment Scheme Collapses

WikiFXRupee Hits Two-Month Low as Oil Surges Past $95

WikiFXWhy RBI Sold $6.1 Billion in Forex Markets in May

WikiFXCNMV Red-Flags 9 Unauthorised Investment Platforms

WikiFXOrder Execution: What Discretionary Latitude Means for Your Trades

WikiFXScammed Twice: Recovery Fraud Takes Advantages of Victims Again

WikiFXWhy Prices Rush Back to Fill Gaps: Liquidity Voids Explained

WikiFXRate Calc