Angel One Review: Regulation, Fees, Platforms, and Risks Explained

Abstract:Angel One review: An India-based unregulated broker with low fees and slick apps with no SEBI or global regulation, raising material investor risk concerns.

Introduction

Angel One is a long-standing India-based brokerage offering equities, F&O, mutual funds, commodities, and access to U.S. stocks, but it operates without SEBI or major global regulatory oversight, creating a pronounced trust and compliance gap despite competitive pricing and capable platforms. Founded in 1996 and positioned around the Angel One Super App, the web-based Angel One Trade, and a developer-focused Smart API, the firm emphasizes usability and product breadth while advertising zero brokerage for the first 30 days up to ₹500. The core issue for risk-minded traders and investors is not functionality or cost, but the absence of a recognized supervisory license, which places counterparty, operational, and recourse risks front and center.

Actionable Takeaways

- Confirm licensing: Verify any SEBI registration and the precise legal entity before account opening or funding.

- Model total cost: Combine brokerage caps with STT, GST, SEBI fees, stamp duty, and applicable daily interest to derive realistic all-in trading costs.

- Match platform to strategy: Mobile for simplicity, web for active trading, and Smart API for programmatic strategies.

- Stress-test risk controls: Without regulator-backed recourse, ensure personal risk management covers counterparty, operational, and margin risks.

What Angel One Offers

Angel One provides multi-asset access across Indian equities, IPOs, F&O, mutual funds, and commodities, plus channels to invest in U.S. equities, covering the typical retail investor journey from onboarding to trading and SIP investing. The lineup is delivered through three main platforms: the Angel One Super App for mobile, Angel One Trade for desktop/web, and Smart API for algorithmic and fintech integrations, addressing beginners through active traders and developers. This breadth positions the broker squarely within Indias mass retail segment, promoting “one-stop” investing and trading with an emphasis on convenience and low entry barriers.

Trading Instruments — Supported

- Stocks — ✓

- IPOs — ✓

- Derivatives (F&O) — ✓

- Mutual Funds — ✓

- Commodities — ✓

- Forex — ✗

- Indices — ✗

- Cryptocurrencies — ✗

- Bonds — ✗

- Options — ✗

- ETFs — ✗

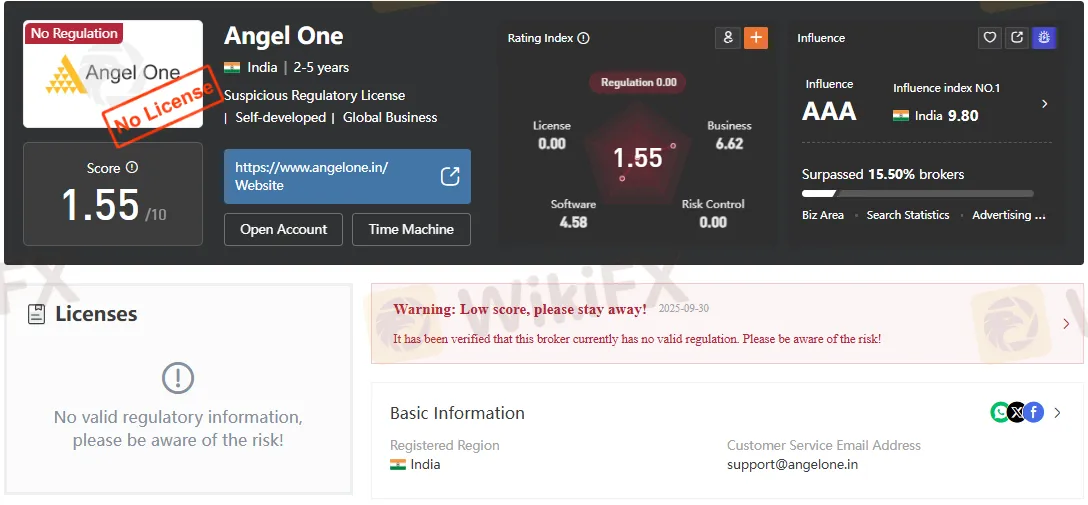

Regulation and Legitimacy

Angel One is not regulated by SEBI or by notable foreign supervisors such as the FCA, ASIC, or NFA, and is described as operating without a controlling financial authority. The material also notes a separate UK company record for a similarly named ANGEL ONE LIMITED that appears deregistered with Companies House details, reinforcing confusion risks around similarly named entities and underscoring the importance of verified licensing. For investors, the practical implication is that dispute resolution, segregation assurances, and prudential safeguards associated with licensed intermediaries may not be available, raising the stakes of counterparty and operational risk.

Fees, Charges, and Pricing

Angel Ones pricing is framed as low to moderate, highlighted by a zero-brokerage introductory offer for the first 30 days, capped at ₹500, before standard capped brokerage applies. Post-offer, equity delivery is charged the lower of ₹20 or 0.1% per order (minimum ₹2), intraday the lower of ₹20 or 0.03% per order, and options at ₹20 per executed order, supplemented by exchange and statutory levies like STT, GST, SEBI fees, and stamp duty per segment. Account costs reflect ₹0 opening, ₹0 AMC for the first year, and thereafter alternatives such as ₹60/quarter for non-BSDA, ₹450/year, or a ₹2950 lifetime plan, with daily interest rates specified for margin funding and debit balances.

Platforms and User Experience

The Angel One Super App targets everyday investors with an accessible mobile interface for equities, mutual funds, and more, while Angel One Trade serves desktop-oriented traders who need fuller depth and tools. Smart API extends the ecosystem to developers and algo traders, enabling programmatic trading and integrations suited to custom strategies and fintech use cases. Marketing materials emphasize high downloads and broad appeal, aligning with India‘s mobile-first investing trend and the platform’s effort to simplify SIPs and multi-asset participation.

Pros, Cons, and Suitability

Key positives include the promotional zero brokerage up to ₹500 in the first 30 days, a broad product shelf covering equities, F&O, mutual funds, commodities, and U.S. exposure, plus a multi-surface platform suite from mobile to web to API. On the downside, the absence of SEBI or global regulatory oversight is a significant red flag, as are the various statutory and service charges that still apply beyond headline brokerage caps. Given these factors, cost-conscious users prioritizing convenience and breadth may see the appeal, but risk-aware investors should weigh the lack of regulation as a decisive factor before committing assets.

Experience and Expert Context

The portfolio of services resembles typical Indian retail brokerage stacks, with SIP-forward messaging and mobile-first utility aligning with market adoption patterns, but the licensing gap remains at odds with best practices for safeguarding client assets. Industry comparisons show that brokers operating under SEBI or top-tier global licenses usually publicize license numbers prominently; the attached profiles explicit “no regulation” status invites enhanced due diligence steps such as segregated funds verification, audited financials, and recovery mechanisms. For traders depending on leverage, margin terms like 0.041% per day for MTF and 0.049% per day for debit balances can materially affect costs in turbulent markets, reinforcing the need for transparent statements and margin risk controls.

Read more

KAMA Capital Review: Do Traders Lose Due to Slippage & Inappropriate Liquidation?

Looking to trade through KAMA Capital, a Mauritius-based forex broker? You must read user reviews concerning fund safety with this brokerage entity. The company, which has been around for two-five years, has received some negative reviews recently for its several trading activities. Users have reported these experiences on broker review platforms such as WikiFX. The negative KAMA Capital reviews highlight serious slippage issues, coupled with inappropriate liquidation issues. The article aims to provide a clear picture of these user allegations along with a regulatory overview of the broker. This will help you make an informed trading decision. Read on!

MTRADING User Reputation: A Deep Look into Real Complaints and Warning Signs

When traders look for information about a broker, their biggest worry is always capital safety. The question, "Is MTRADING safe or scam?" gets right to the point. Based on checkable information from worldwide broker regulatory websites, the answer comes with serious warnings. MTRADING operates with major warning signs, especially a status of "No Regulation" and a very low trust score. WikiFX, a third-party checking service, gives the broker an extremely low rating and clearly warns of "High potential risk". This article will break down the proof behind this conclusion. We will look at MTRADING's regulatory status, examine real user complaints recorded on public websites, and check its platform features to give a clear, fact-based view for any potential user.

MTRADING Legitimacy Check: Is This a Fake Broker or a Legitimate Trading Partner?

You're asking 'Is MTRADING legit?' or worried about an 'MTRADING scam', and that's the right question to ask before risking your funds. A deep look into MTRADING's background shows major warning signs that should make you very careful. This isn't a simple yes or no answer; it's a fact-based review of the risks. Our research, using data from independent broker checking websites like WikiFX, shows MTRADING has a very low score, which means there are serious problems. The main worries are about whether it's properly regulated and the troubling number of customer complaints.

Core Prime Withdrawal & Deposit: What You MUST Know Before Funding Your Account

For any trader, understanding how to move funds is extremely important. How you add funds to your account and, more importantly, how you take them out, including the profits earned on the platform, can shape your entire trading experience. You are likely here looking for specific information about Core Prime deposit and Core Prime withdrawal methods. This guide will explain the payment options the broker claims to offer. However, knowing the process is only part of the story. The other, more important part involves understanding the risks and whether the broker can be trusted. A nice-looking website and many payment options mean nothing if your capital is not safe. The main question we need to ask is not just *how* you can withdraw funds, but *if* you can. Can you trust that your funds will be safe and your withdrawal requests will be processed? Let's look at the facts.

WikiFX Broker

Latest News

MTRADING Legitimacy Check: Is This a Fake Broker or a Legitimate Trading Partner?

WikiFX

WikiFXTrilt Review 2025: Is This Forex Broker Safe?

WikiFX225 People Investigated as Singapore Losses Exceed S$4.8 Million

WikiFXLuxury Villas in Sabah Raided, 28 Foreign Suspects Arrested

WikiFXWhy Smart Beginners Keep Blowing Up Their Forex Accounts

WikiFX中海寰球 Review 2026: Severe Risk Signals and Unregulated Status

WikiFXXTRADE Review 2025: Is This Forex Broker Safe?

WikiFXKAMA Capital Review: Do Traders Lose Due to Slippage & Inappropriate Liquidation?

WikiFXTradeZero Review 2026: Should You Trade With This Broker?

WikiFXCryptomaxtrade Review 2026: Unregulated Status, Low Score, and Key Warnings

WikiFXRate Calc