Japanese Yen Eases on BoJ Dovish Statement

Abstract:The Japanese Yen eased on Wednesday morning after the BoJ Deputy Governor indicated that the Japanese central bank would not raise interest rates if global markets remained unstable. This statement has calmed the market and unwound concerns about Yen carry trades. Meanwhile, the dollar has regained strength, with the dollar index (DXY) climbing above the $103 mark.

Japanese Yen eased in strength as the market reacted to BoJ Dovish tone.

Upbeat job data and Speculative hawkish monetary policy from RBNZ stimulate the New Zealand Dollar.

Equity markets have signs of recovery from their recent sell-down.

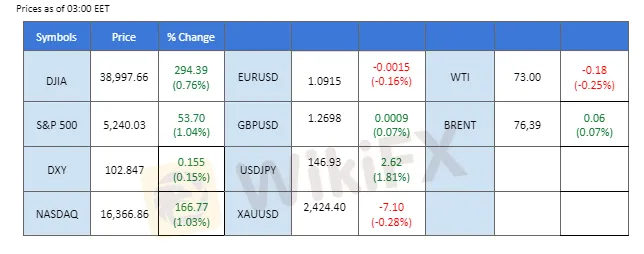

Market Summary

The Japanese Yen eased on Wednesday morning after the BoJ Deputy Governor indicated that the Japanese central bank would not raise interest rates if global markets remained unstable. This statement has calmed the market and unwound concerns about Yen carry trades. Meanwhile, the dollar has regained strength, with the dollar index (DXY) climbing above the $103 mark.

Additionally, the New Zealand dollar is in focus as today's New Zealand job data exceeded market expectations, showing an improved unemployment rate and higher wage growth. This suggests that the Reserve Bank of New Zealand may maintain its current restrictive monetary policy for an extended period.

In the equity markets, global equities are expected to ease from recent selling pressure as financial institutions may start buying the dip, providing support for the markets. Asian markets began the day with positive gains, a sentiment likely to be shared with the U.S. market later in the day.

In the commodity market, gold is under pressure due to the strengthening dollar and the rebound in U.S. Treasury yields. Oil prices remain lacklustre as concerns persist over the pessimistic economic outlook and a surprise buildup in U.S. crude stockpiles, as indicated by last night's data.

Current rate hike bets on 18th September Fed interest rate decision:

Source: CME Fedwatch Tool

0 bps (88.5%) VS -25 bps (11.5%)

Market Overview

Economic Calendar

(MT4 System Time)

Source: MQL5

Market Movements

DOLLAR_INDX, H4

With expectations that the Federal Reserve might cut interest rates aggressively, US Treasury 10-year yields are trending downward. Dovish expectations from the Fed have weighed on the appeal of the US Dollar. While some investors re-entered the dollar market post-stabilization, mostly due to dip buying, the longer-term trend for the dollar remains bearish. Downbeat economic performance and Fed rate cut expectations are likely to continue weighing on the demand for the dollar.

The Dollar Index is trading higher following the prior rebound from the support level. MACD has illustrated diminishing bearish momentum, while RSI is at 36, suggesting the index might experience technical correction since the RSI rebounded sharply from oversold territory.

Resistance level: 104.05, 106.05

Support level: 102.40, 100.90

XAU/USD, H4

Gold prices extended their losses as investors sold off gold to convert it into cash to cover margin calls from banks. Following the global equity market and crypto asset selloff, investors shifted their portfolios to these asset classes for dip-buying opportunities. The potential for a trend reversal in the gold market remains data-dependent and influenced by monetary policy expectations. Investors should continue monitoring these catalysts for further trading signals.

Gold prices are trading lower while currently testing the support level. MACD has illustrated increasing bearish momentum, while RSI is at 39, suggesting the commodity might extend its losses after breakout since the RSI stays below the midline.

Resistance level: 2415.00, 2450.00

Support level: 2380.00, 2355.00

GBP/USD,H4

Pound Sterling eased in strength as the country faced social uncertainty due to ongoing riots. Anti-immigrant riots in multiple cities across the U.K. have dented confidence in Sterling. Meanwhile, the U.S. dollar regained strength, bolstered by an improvement in U.S. Treasury yields exerting downside pressure on the pair.

GBP/USD has recorded four weeks of straight decline and is trading toward its lowest level since June, suggesting a bearish bias for the pair. The RSI remains close to the oversold zone, while the MACD has a bearish cross and is edging lower, suggesting the pair remains trading with bearish momentum.

Resistance level: 1.2780, 1.2850

Support level: 1.2630, 1.2550

EUR/USD,H4

The EUR/USD pair faced profit-taking sentiment after surpassing the 1.1000 mark and is struggling to sustain above the next support level near 1.0900. A break below this level would suggest a solid bearish bias for the pair. The euro's strength was hindered by disappointing eurozone Retail Sales figures released yesterday, while the U.S. dollar index reclaimed its $103 territory last night, exerting further downside pressure on the pair.

The pair continues to trade in a downtrend trajectory since it hit its highest level in 2024. The RSI has dropped out from the overbought zone while the MACD has a bearish cross and is edging lower suggest the bullish momentum is easing.

Resistance level: 1.0940, 1.0985

Support level: 1.0895, 1.0853

USD/JPY, H4

The Japanese Yen traded softer after the BoJ released a dovish statement, leading the USD/JPY pair to rebound sharply from its recent bearish trend. The BoJ Deputy Governor claimed that the Japanese central bank would not raise interest rates further if the markets are unstable, which calmed market unease regarding the Yen carry trade.

The pair has rebounded by more than 3% from its recent low level near the 141.80 mark. The RSI has surged sharply from the oversold zone, while the MACD has a bullish cross and is edging toward the zero line from below, suggesting the bearish momentum is easing.

Resistance level: 148.65, 150.10

Support level: 145.27, 143.55

NZD/USD, H4

The NZD/USD pair surged sharply during Wednesday's Sydney session after the release of New Zealand's job data. The data exceeded market expectations, showing an improved unemployment rate and heightened wage growth. This suggests that the Reserve Bank of New Zealand (RBNZ) may stick with its current monetary tightening policy, bolstering the Kiwi's strength.

The pair has broken above its resistance level at 0.5960, suggesting a trend reversal signal. The RSI has been flowing above the 50 level, while the MACD was supported above the zero line, suggesting the pair is trading with bullish momentum.

Resistance level: 0.6020, 0.6080

Support level: 0.5910, 0.5860

S&P 500, H4

The global financial market began stabilising after the aggressive selloff on Monday. Hedge funds and institutional investors bought the dip, supporting the equity market. The S&P 500 index rebounded by 1% on Tuesday after experiencing its worst session in almost two years. Wall Streets chief fear gauge, the CBOE VIX Index, fell from its highest level since 2020 as the market began to digest the previous volatility.

S&P 500 is trading higher following the prior rebound from the support level. MACD has illustrated diminishing bearish momentum, while RSI is at 35, suggesting the index might experience technical correction since the RSI rebounded sharply from oversold territory.

Resistance level: 5400.25, 5670.00

Support level: 5150.00, 4949.70

Read more

Wall Street Rally on Soft CPI

The most anticipated economic indicator of the week, the U.S. Consumer Price Index (CPI), was released yesterday, coming in at 2.9%, below the 3% threshold and in line with the Producer Price Index (PPI) data from the previous day. This further sign of easing inflationary pressure in the U.S. has heightened expectations that the Federal Reserve may implement its first rate cut in September.

Wall Street Advances Ahead of CPI

The equity markets continued their upward momentum, driven by the easing of the Japanese Yen's strength. The Yen was pressured by a dovish tone from Japanese authorities, signalling that the Bank of Japan (BoJ) might keep its monetary policy unchanged amid rising global economic uncertainties.

Nasdaq Bullish, Encourage by Upbeat U.S. Job Data

The financial markets reacted positively to the upbeat Initial Jobless Claims data released yesterday, which came in at 233k, lower than market expectations. This eased concerns about a weakening labour market and the heightened recession risks that emerged after last Friday's disappointing NFP report. Wall Street benefited from the improved risk appetite, with the Nasdaq leading gains, surging by over 400 points in the last session.

Dovish Fed’s Statement Hammers Dollar

The highly anticipated Fed’s interest rate decision was disclosed yesterday, hammering the dollar’s strength lower as Fed Chief Jerome Powell explicitly signalled that a September rate cut is possible. The U.S. central bank is balancing both inflation and recession risks, with interest rates adjusted to curb inflation while maintaining a solid labour market.

WikiFX Broker

Latest News

LQH MARKETS Review: Multiple Traders Report Withdrawals Blocked and Accounts Terminated

WikiFX

WikiFXSpread Cheating: The Invisible Trading Cost That Could Be Working Against You

WikiFX"They Want to See Your Face": Inside ATFX Cambodia's Rise

WikiFXTrump Memecoin Faces SEC Scrutiny After Nearly One Million Investors Suffer Heavy Losses

WikiFXApple Faces Lawsuit Over Fake Crypto App Exposing $1.8 Million Theft

WikiFXBorn2trade Adds Copy Trading to 1:5000 Leverage Platform

WikiFXLevels Review: No Regulation and Mounting Withdrawal Complaints – What Traders Need to Know

WikiFXPILOTFX Review: What Traders Should Know Before Depositing

WikiFXLMAX Group Review 2026: Users Report Disturbing Withdrawal Issues - Is the Broker Still Reliable?

WikiFXLuno Review: Unregulated Broker Warning After Frozen Accounts and Blocked Withdrawals

WikiFXRate Calc