Mohicans markets:MHM Today’s News

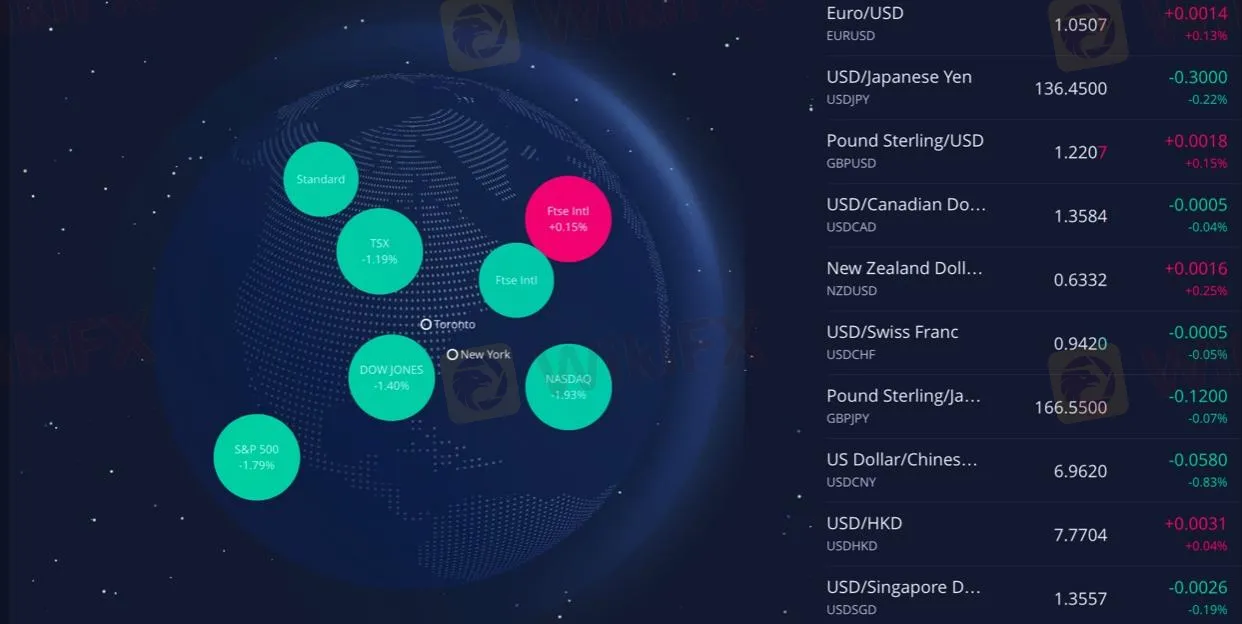

Abstract:On Monday, December 5, a number of better-than-expected U.S. data reinforced expectations that the Fed would keep tightening, and the dollar index rebounded to above 105, closing up 0.75% at 105.29. Non-dollar currencies continued to fall, with AUD/USD down 1.50% during the day, USD/CAD up to 1.36, EUR/USD down 1.05, USD/JPY up 1.50% during the day, both offshore and onshore RMB recovered 7.0 level.

![第一篇[英语]](https://d126a7rrmtfkku.cloudfront.net/fb_article/2022-12-06/638059350736116774/FB638059350736116774_490461.jpg-article598)

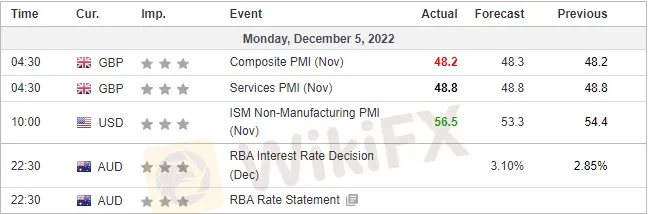

December 6, 2022-Fundamental Reminder

☆ 11:30 The Australian Federal Reserve announces its interest rate resolution.

☆ 23:00 U.S. releases the New York Fed Global Supply Chain Stress Index for November.

☆ The following day 01:00 EIA releases its monthly short-term energy outlook report.

☆ The following day 05:30 U.S. releases API crude oil inventories for the week ending Dec. 2.

MHMarkets -Market Overview

Review of Global Market Trend

On Monday, December 5, a number of better-than-expected U.S. data reinforced expectations that the Fed would keep tightening, and the dollar index rebounded to above 105, closing up 0.75% at 105.29. Non-dollar currencies continued to fall, with AUD/USD down 1.50% during the day, USD/CAD up to 1.36, EUR/USD down 1.05, USD/JPY up 1.50% during the day, both offshore and onshore RMB recovered 7.0 level.

U.S. bonds extended their intraday decline, with the 2-year U.S. bond yield rising to a maximum of 4.42% and closing trading near 4.4%; the 10-year U.S. bond yield touched 3.61%, which was up more than 10 basis points. The inversion of the U.S. 2-10 year Treasury yield reached 81.8 basis points, which was the largest inversion since 1981.

Spot gold fell below $1,770 per ounce, and spot silver fell more than 4% intraday. By the close of trading, spot gold closed down 1.61% at $1,768.82 per ounce, while spot silver closed down 3.87% at $22.25 per ounce.

Crude oil continued to fall after rising more than 3% intraday, with WTI crude once plunging 4% to close down 3.56% at $77.35 per barrel; Brent crude lost $84 per barrel to close down 3.35% at $83.02 per barrel. U.S. natural gas fell more than 11 percent to a new low of more than a month.

U.S. stocks opened lower, extending losses after Russia accused Ukraine of attacking a Russian military airport. By the close of trading, the Dow Jones closed down 1.40%, the S&P 500 closed down 1.79% and the Nasdaq Composite Index closed down 1.93%. The energy and finance sectors were the top losers, with Tesla closing down 6.37%.

European stocks generally closed lower, Germany's DAX30 index closed down 0.56%, the FTSE 100 index closed up 0.17%, France's CAC40 index closed down 0.67%, the European Stoxx 50 index closed down 0.53%, Spain's IBEX35 index closed down 0.13%, and Italy's FTSE MIB index closed down 0.29%.

Hot Spots in the Market

1. The strong US ISM non manufacturing PMI and other data triggered the market's concern about the Fed's interest rate hike. The Nasdaq Composite Index gave up its gains last week on Monday, and the 2Y/10Y upside down deepened to 82BP. The market expected the Fed's terminal interest rate to return to 5%, about 10BP higher than the previous trading day.

2. The EU and the United States committed to resolving the differences on subsidies in the “Inflation Reduction Act”.

3. Bank for International Settlements: According to the off balance sheet report, the foreign exchange swap position shows that the hidden US dollar debt exceeds 80 trillion US dollars.

4. Saudi Arabia lowered the price of most oil sold to Asia in January to 3.25 dollars per barrel of premium.

5. American Energy Security Envoy Hochstein: There is still enough strategic oil reserves to deal with emergencies.

6. Financial Times: The UK has finalized the regulatory plan for the cryptocurrency industry.

7. The Biden government will hold an online meeting with American oil executives on December 8 to discuss how to support Ukraine's energy infrastructure. The US Energy Secretary will meet with many oil company executives on the 14th.

8. Russian Ministry of Defense: Two military airports in Russia were attacked by Ukraine, causing 3 deaths and 4 injuries. A few hours later, Ukraine reported that Russia had launched a new round of missile attacks.

Geopolitical situation

Conflict situation:

1. Russian Ministry of Defense: two military airports in Russia were attacked by Ukraine, causing 3 deaths and 4 injuries; A few hours later, Ukraine reported that Russia had launched a new round of missile attacks; Ukrainian officials said Ukraine used drones to attack two bases in central Russia.

2. The Donetsk side said that Uzbek troops shelled Donetsk territory 34 times in the past day and fired more than 150 rounds of ammunition.

3. Ministry of National Defense of Ukraine: Russian missile attacks have disrupted the process of redeployment of Ukraine's armed forces reserves, foreign weapons, military equipment and ammunition to the operational areas by rail.

4. Moldova found a missile falling on its border with Ukraine.

5. The Governor of Kiev, Ukraine: Some infrastructure in the region was hit by Russian missiles, and 40% of the places had no electricity, but there were no “serious consequences”.

Energy situation:

1. The White House of the United States said that Biden would not consider using Russian oil to supplement strategic oil reserves.

2. The Kremlin: Russia is ready to respond to the introduction of an oil price ceiling by the West; Russia will not recognize the decision of the West.

3. Due to the fact that some power stations cannot operate at full load, coupled with cooling and other factors, there will be power shortage in the next day, so Ukraine will implement emergency power rationing measures.

4. Türkiye requires the tanker to re enter the risk, and tanker congestion occurs in the Türkiye Strait.

MHMarkets-Institutional Perspective

1. Goldman Sachs:The US Treasury may not be able to achieve its year-end cash balance target

2. SOCIETE GENERALE:The recent rebound in US debt may not indicate an improvement in the situation

3. MUFG:Bank of Canada may strengthen Canadian dollar weakness

Statement | Disclaimer

Disclaimer: The information contained in this material is for general consultation only. It does not take into account your investment objectives, financial situation or special needs. We have made every effort to ensure the accuracy of the information as of the date of publication. MHMarkets makes no warranty or representation on this material. The examples in this material are for illustrative purposes only. To the extent permitted by law, MHMarkets and its employees shall not be liable for any loss or damage arising from any information provided or omitted in this material in any way (including negligence). The characteristics of MHMarkets' products, including applicable fees and charges, are outlined in the product disclosure statement provided on MHMarkets' website. Derivatives may be risky; The loss may exceed your initial payment. MHMarkets recommends that you seek independent advice.

MohicansMarkets, (abbreviation: MHMarkets or MHM, Chinese name: Maihui), Australian Financial Services License No. 001296777.

Read more

Mohicans markets:MHM European Market

Spot gold weakened slightly during the Asian session on Thursday (April 6), hitting a two-day low of $2007.89 per ounce and now trading near $2014.15. A series of weak economic data has fueled fears of an impending recession in the US, giving safe-haven support to the dollar. And some dollar shorts took profits, and gold bulls also took profits ahead of Good Friday and the non-farm payrolls data, putting pressure on gold prices.

Mohicans markets:MHM Today News

On Wednesday, as the less-than-expected March "ADP" data and non-manufacturing PMI data fueled market concerns about an economic slowdown and spurred bets that the Federal Reserve could slow interest rate hikes. Spot gold continued to brush a new high since March last year, which was the highest intraday to $2032.13 per ounce, and then retracted most of the day's gains, finally closing up 0.01% at $2020.82 per ounce; spot silver hovered around $25 during the day, finally closing down 0.21% at $2

Mohicans markets:MHM European Market

Spot gold oscillated slightly lower during the Asian session on Tuesday (April 4) and is currently trading around $1980.13 per ounce. The dollar index rebounded mildly after a big drop overnight, putting pressure on gold prices. However, this week will see the non-farm payrolls report, there is no important economic data out on Tuesday, and the market wait-and-see sentiment is getting stronger.

Mohicans markets :MHM Today News

On Monday, in OPEC + members unexpectedly cut production reignited market concerns about long-term inflation and sparked uncertainty about the Fed's response, the dollar index once up to the 103 mark, and then on a "vertical roller coaster", giving back all the gains of the day and once lost 102 mark, finally closed down 0.53% at 102.04; U.S. 10-year Treasury yields rose and then fell, as data showed that the U.S. economy continues to slow, it fell sharply in the U.S. session, and once to a low

WikiFX Broker

Latest News

Balancing Chart Volatility With Account Limits in Stop Loss Placement

WikiFX

WikiFXHTFX Review 2026: Withdrawal Complaints, Offshore Regulation, and Account Access Risks

WikiFXThe Dunning-Kruger Trap: How Beginner Forex Traders Can Overcome Overconfidence and Manage Risk

WikiFXUnderstanding Currency Pairs, Central Banks and Core Forex Market Risks

WikiFXVantage Review 2026: Is This Forex Broker Safe?

WikiFXCFI Review 2026: Should You Trade with This Broker?

WikiFXInteractive Brokers Review 2026: Regulation Fines, Platform Access, and Complaint Risks

WikiFXPepperstone Review 2026: Massive Deposit & Withdrawal Complaints Against This Regulated Broker

WikiFXWhat Beginners Must Know About Stop-Loss Orders and Trading Risk

WikiFXReview 2026: Deriv Regulation, Complaints, and Withdrawal Risk Signals

WikiFXRate Calc