SBM

Abstract: Headquartered in Mumbai, India, SBM Bank offers online banking services. SBM Bank India provides a comprehensive portfolio, serving retail, MSMEs, NRIs, and corporate clients with a full slate of banking services including savings/current accounts, fixed/recurring deposits, loans, credit and debit cards, trade finance, treasury, and digital banking.

| SBM Review Summary | |

| Founded | 2016 |

| Registered Country/Region | India |

| Regulation | No Regulation |

| Platform/APP | SBM baking platform |

| Customer Support | Contact Form |

| Phone: 1800 2099 335, 1800 1033 817 | |

| Email: customercare@sbmbank.co.in | |

| Social Media: Facebook, Instagram, YouTube, LinkedIn, Twitter, WhatsApp | |

| Company Address: 306–A, the Capital, G block, Bandra-Kurla Complex, Bandra East, Mumbai 400051, Maharashtra | |

SBM Information

Headquartered in Mumbai, India, SBM Bank offers online banking services. SBM Bank India provides a comprehensive portfolio, serving retail, MSMEs, NRIs, and corporate clients with a full slate of banking services including savings/current accounts, fixed/recurring deposits, loans, credit and debit cards, trade finance, treasury, and digital banking.

Pros and Cons

| Pros | Cons |

| Multiple account types | No regulation |

| Various types of deposit options | Lack of transparency |

| Unclear fee structure |

Is SBM Legit?

No. SBM Bank is operating without regulatory supervision, which indicates that investing in this platform can be risky.

Account Type

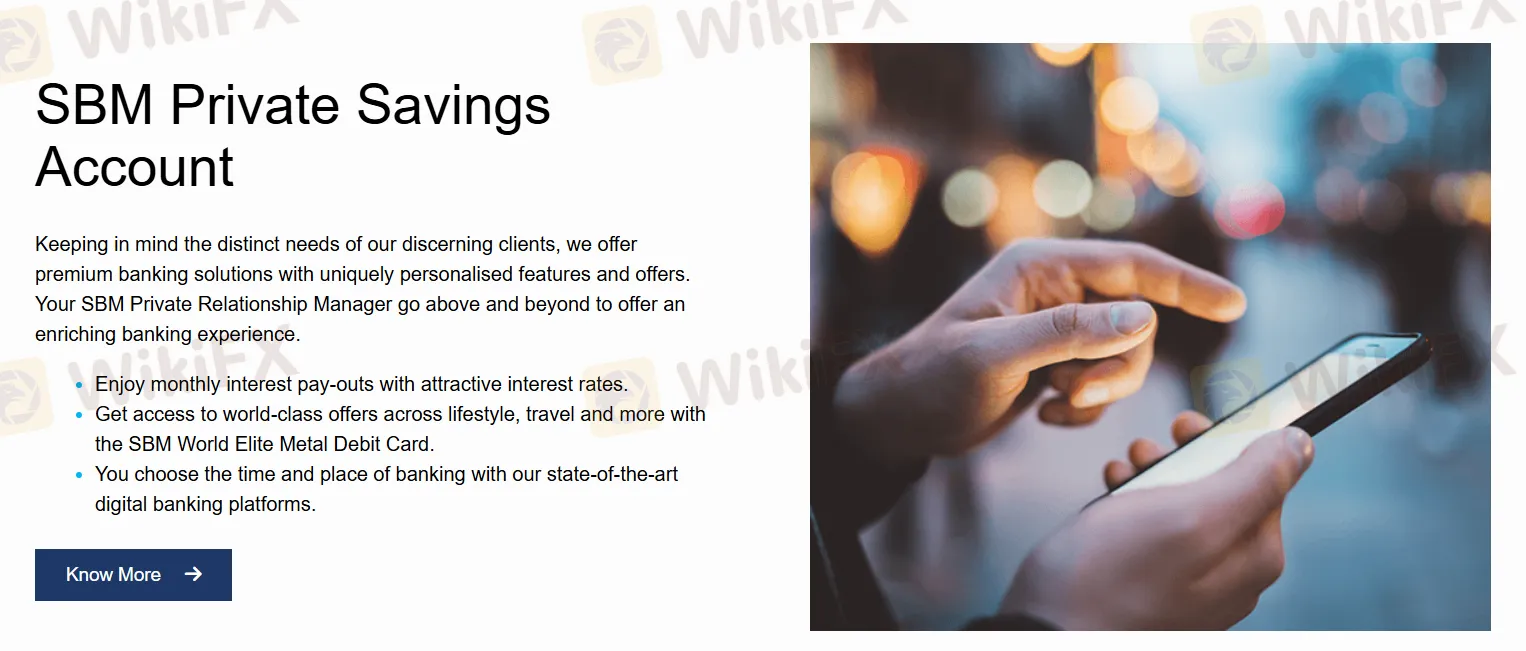

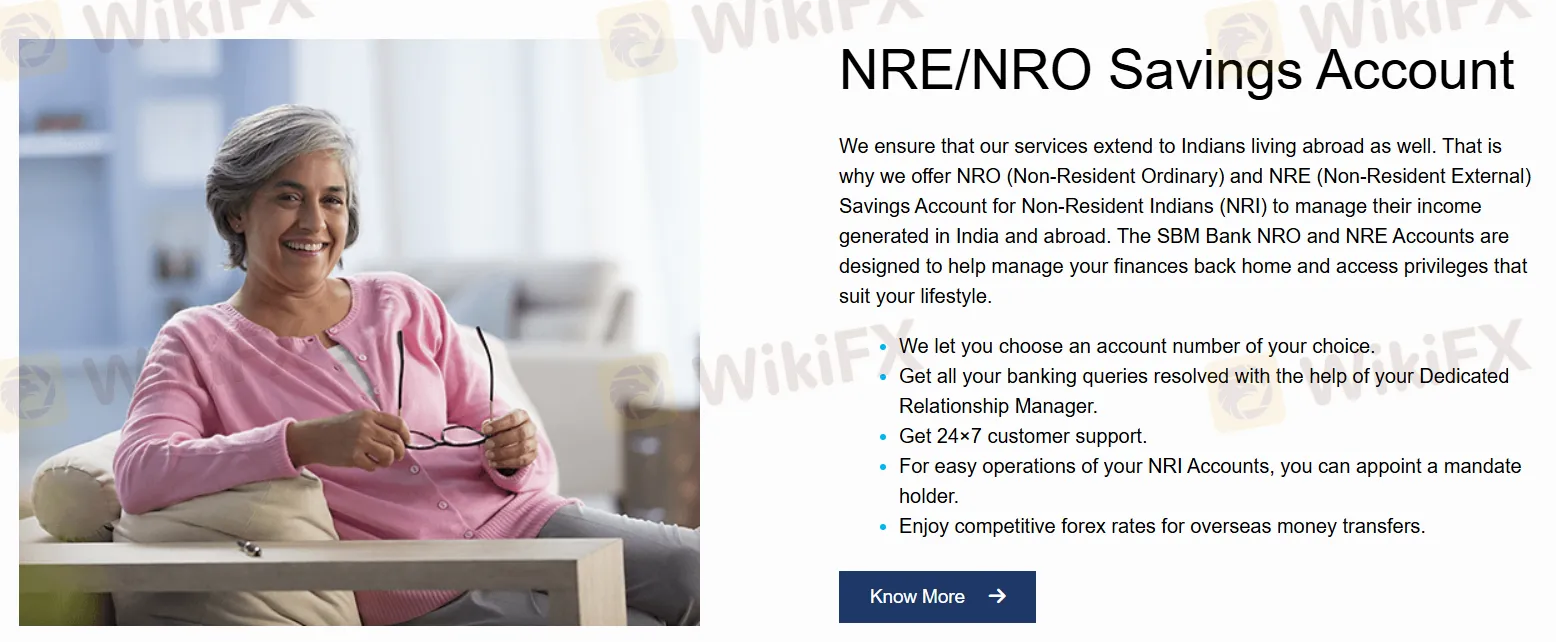

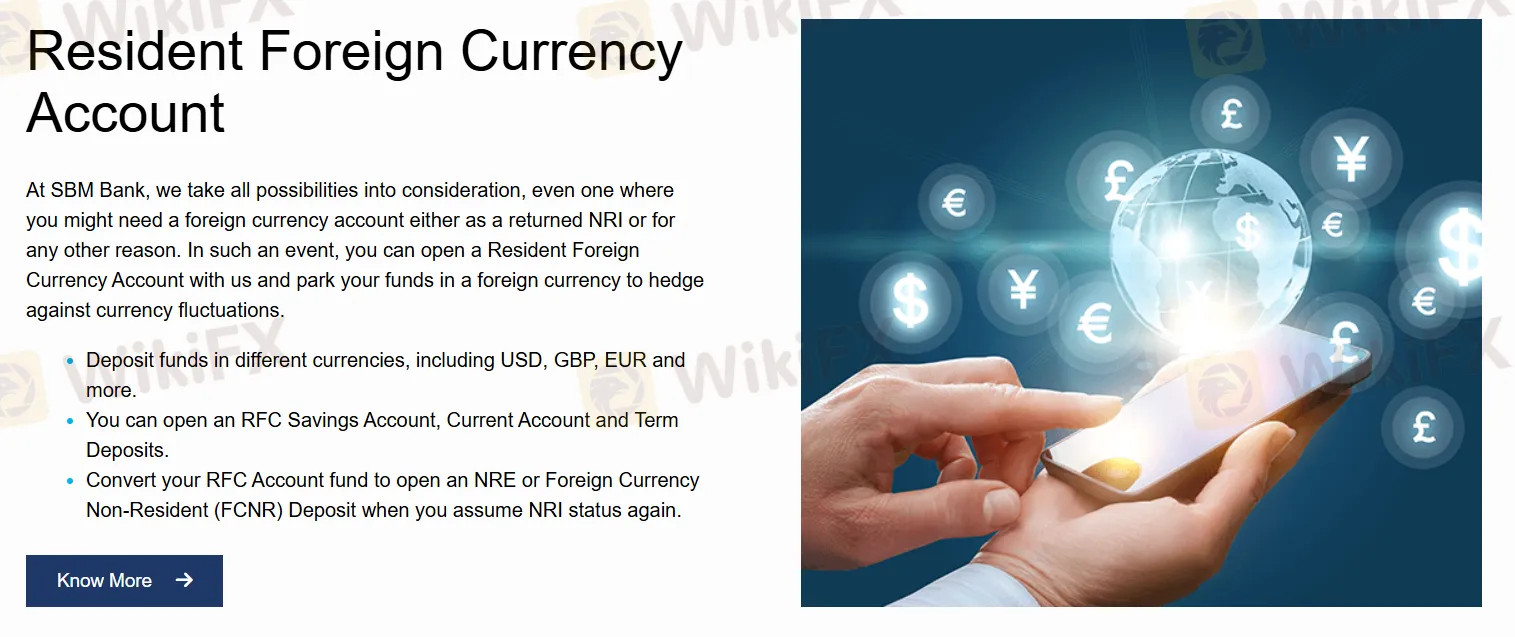

SBM Bank provides a variety of bank accounts, including the SEM Wealth Savings Account, SEM Private Savings Account, NRE/NRO Savings Account, Resident Foreign Currency Account, and Overseas Account. Each account is tailored to meet the needs of a specific type of investor and comes with its own unique set of features.

SEM Wealth Savings Account:

- Enjoy unlimited free withdrawals and deposits, along with unlimited cash withdrawals at all bank ATMs.

- Receive monthly interest payouts.

- Experience premium benefits with the VISA Signature Debit Card.

- Select a custom account number of your choice.

- Wealth Management services.

SEM Private Savings Account:

- Earn monthly interest payouts with competitive interest rates.

- Access premium global offers on lifestyle, travel, and more through the SBM World Elite Metal Debit Card.

- Bank anytime and anywhere with ease using SEM's advanced digital banking platforms.

NRE/NRO Savings Account:

- You get to choose the account number of your choice.

- Get all your banking queries resolved with the help of your Dedicated Relationship Manager.

- 24/7 customer support.

- For easy operations of your NRI Accounts, you can appoint a mandate holder.

- Enjoy competitive forex rates for overseas money transfers.

Resident Foreign Currency Account:

- Deposit funds in different currencies, including USD, GBP, EUR and more.

- You can open an RFC Savings Account, a Current Account and Term Deposits.

- Convert your RFC Account fund to open an NRE or Foreign Currency Non-Resident (FCNR) Deposit when you assume NRI status again.

Overseas Account:

- Enjoy attractive interest rates.

- Open an account in your preferred foreign currency.

- Access a multitude of global investment opportunities.

- Enjoy competitive foreign currency exchange rates for international transactions.

Trading Platform

SBM claims to provide advanced digital banking platforms.

Deposit and Withdrawal

At SEB Bank, you get access to various types of deposit options.

Fixed Deposit: It enables you to invest funds for a pre-decided tenure and earn interest at a pre-determined rate. You can select the interval at which you wish to receive interest payouts, and you will receive the principal amount upon maturity.

NRO/NRE Fixed Deposit: Designed for Non-Resident Indians, an NRO/NRE Fixed Deposit allows Indians living abroad to invest their wealth and earn attractive returns. While an NRO FD allows NRIs (Non-Resident Indians) to invest the income earned in India, an NRE FD is geared towards earnings generated abroad.

Tax-Saving Fixed Deposit: A Tax-Saving Fixed Deposit would help you if hefty taxes are your concern. Apart from providing the benefits of a regular FD, a Tax-Saving Fixed Deposit also helps you claim deductions that go a long way in helping you plan and save on taxes.

Recurring Deposit: A Recurring Deposit is a unique deposit that enables you to earn interest while depositing funds regularly. With savings, additional income, and flexibility on the cards, an RD is an important investment tool to have in your portfolio.

Read more

Exchange Rate Fluctuations: Key Facts Every Forex Trader Should Know

The forex market is a happening place with currency pairs getting traded almost non-stop for five days a week. Some currencies become stronger, some become weaker, and some remain neutral or rangebound. If you talk about the Indian National Rupee (INR), it has dipped sharply against major currencies globally over the past year. The USD/INR was valued at around 85-86 in Feb 2025. As we stand in Feb 2026, the value has dipped to over 90. The dip or rise, whatever the case may be, impacts our daily lives. It determines the price of an overseas holiday and imported goods, while influencing foreign investors’ perception of a country. The foreign exchange rates change constantly, sometimes multiple times a day, amid breaking news in the economic and political spheres globally. In this article, we have uncovered details on exchange rate fluctuations and key facts that every trader should know regarding these. Read on!

Is Forex Still Worth It in 2026? Global Central Banks Are Splitting

Entering 2026, diverging central bank policies are reshaping global FX and bond markets, while economic momentum shifts from developed economies toward India. Meanwhile, an upcoming leadership transition at the US Federal Reserve presents a key underappreciated risk that could trigger renewed volatility in interest rates and the US dollar.

US-China Tariffs Heat Up—Pause Still Possible, Says Bessent

President Trump signaled the U.S. and China are effectively in a trade war, even as Treasury Secretary Scott Bessent left room to extend a current tariff pause and a Trump–Xi meeting remains on the calendar. After floating a new 100% tariff on Chinese goods from Nov. 1, tensions seesawed amid Chinese sanctions and U.S. threats over soybeans. Some U.S. tariffs (up to ~145%) are paused until Nov. 10, with a Supreme Court test of “reciprocal” tariffs looming. Companies are adapting unevenly—Stellantis expanding in the U.S., while Apple deepens ties in China—suggesting continued market volatility.

Crypto, Euro, Yuan: Still No Dollar Killer

Despite frequent “de-dollarization” headlines, the U.S. dollar remains unrivaled due to unmatched market depth, global usability, and trusted legal/institutional frameworks. Crypto and other currencies (euro, yuan) lack the stability, convertibility, and infrastructure required to replace the USD, while the Fed’s credibility and the scale of U.S. financial markets continue to anchor demand. Bottom line: no alternative currently offers a complete, credible substitute for the dollar’s global role.

WikiFX Broker

Latest News

WHITEFOREX Review 2026: I Am Not the Only Victim of Its Profit Seizure Activity; Users Say This!

WikiFX

WikiFXVonway Forex Review: No Regulation, Withdrawal Complaints, and a Broker Warning

WikiFXFinalto Review 2026: Regulation, Trading Environment, and Platform Access Risks

WikiFXReview 2026: TRADING 212 Regulation, Clone Warning, and Withdrawal Complaint

WikiFXReview 2026: BOLD PRIME Complaints, Regulation Warnings, and Withdrawal Risk

WikiFXReview 2026: EMIRAX MARKETS Regulation, Withdrawal Complaints, and Trading Risks

WikiFXPolymarket Under Fire as Wall Street Watchdog Launches Investigation

WikiFXRoboMarkets Review 2026: Regulation, Complaints, and Execution Quality

WikiFXMazi Finance Review 2026: Unregulated Status, Withdrawal Complaints, and Risk Signals

WikiFX⚽💱 World Cup · Forex Predict & Win Event

WikiFXRate Calc